Toll Free 1800 572 9282

Toll Free 1800 572 9282  mailus@wbcsmadeeasy.in

mailus@wbcsmadeeasy.in

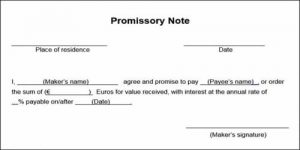

W.B.C.S. Examination Notes On – Promissory Note – Commerce And Accountancy Notes.

The promissory note is defined as an instrument in writing (not being a banknote or a currency note), containing an unconditional undertaking signed by the maker, to pay a certain sum of money only to or to the order of a certain person, or to the bearer of the instrument.Continue Reading W.B.C.S. Examination Notes On – Promissory Note – Commerce And Accountancy Notes.

Importance of Promissory note in Bill of Exchange

According to the Negotiable Instruments Act 1881, the meaning of promissory note is ‘an instrument in writing (not being a banknote or a currency note), containing an unconditional undertaking signed by the maker, to pay a certain sum of money only to or to the order of a certain person, or to the bearer of the instrument. However, according to the Reserve Bank of India Act, a promissory note payable to bearer is illegal. Therefore, a promissory note cannot be made payable to the bearer.’

Parties to a Promissory Note

There Are Two Parties to a Promissory Note:

(1) Maker: Maker or drawer is an individual or entity who makes or draws the promissory note with a promise to pay a certain sum as is specified in the promissory note. Maker is also known as promsior.

(2) Payee: The payee is the person in whose favour the promissory note is drawn.

| (a) Term of Bill or Period of Bill | It is the time period between the date on which a bill is drawn and the date on which it is payable. |

| (B) Due Date | It is the date on which the payment of the bill is due. |

| (C) Days of Grace | These are the three extra days added to the period of bill. |

| (D) Date of Maturity | The date which comes after adding three days of grace to the period of bill. |

Please subscribe here to get all future updates on this post/page/category/website